If you are considering buying a cabin cruiser in Florida, one of the most important long term expenses you need to understand is insurance. While many first time buyers focus on purchase price, fuel, and dockage, insurance is what protects your investment when the unexpected happens.

After years in the boating industry and owning multiple vessels in South Florida, I can tell you that yacht insurance is not something you want to treat as an afterthought. The right policy can save you tens of thousands of dollars after a storm, collision, theft, or mechanical failure.

In this guide, I will walk you through the average insurance cost for a 35 foot cabin cruiser in Florida, what affects your premium, how to lower your rates, and what coverage you actually need.

If you are serious about responsible yacht ownership, understanding insurance is part of doing it right.

For most owners in South Florida, the average insurance cost for a 35 foot cabin cruiser falls within the following range:

For most responsible owners who want solid protection, the realistic average is $2,500 to $3,200 per year.

This range reflects real world pricing for vessels kept in Florida marinas, used year round, and operated in coastal and offshore waters.

Florida consistently ranks as one of the most expensive states for boat insurance.

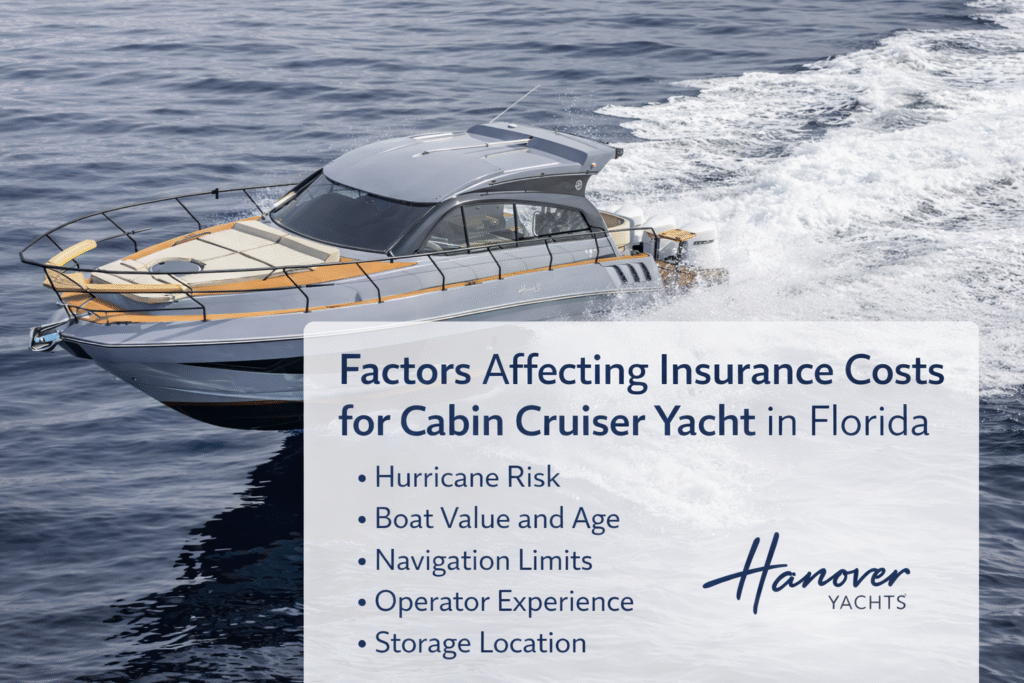

Hurricane exposure plays a major role in pricing. Insurers must account for large scale storm losses that occur regularly in coastal regions.

High vessel density in South Florida increases the likelihood of accidents and liability claims. More boats in limited waterways create higher risk.

Year round boating activity means constant exposure. Boats are not stored for winter, which reduces wear in northern states.

Saltwater conditions accelerate corrosion and mechanical wear, leading to more frequent claims.

These factors combine to raise premiums across the state.

Insurance companies evaluate multiple variables when setting your premium.

Boat value is one of the biggest factors. Higher priced vessels cost more to insure.

Hull design and construction quality affect long term durability and repair costs.

Engine configuration matters. Twin engine boats generally cost more to insure.

Storage location plays a major role. Boats kept in protected marinas or dry storage receive lower rates.

Navigation limits determine where you are allowed to operate. Offshore and international coverage increases premiums.

Operator experience reduces risk. Documented boating history leads to better pricing.

Claims history directly affects your rate. Prior claims usually result in higher premiums.

A well structured cabin cruiser policy includes several essential protections.

Hull and machinery coverage protects the physical vessel, engines, and onboard systems.

Liability coverage pays for property damage and bodily injury to others. Most policies provide $300,000 to $1 million in protection.

Personal property coverage insures electronics, fishing gear, and accessories.

Salvage and wreck removal covers the cost of recovering damaged vessels.

Pollution liability protects against fuel spill cleanup expenses.

Medical payments cover injuries to passengers and crew.

Comprehensive coverage should include all of these elements.

Understanding valuation is critical when selecting insurance.

Agreed value policies guarantee a fixed payout with no depreciation. Premiums are higher, but protection is stronger.

Actual cash value policies depreciate over time and offer lower premiums. Payouts are reduced as the boat ages.

Most experienced owners prefer agreed value coverage, especially for newer yachts.

Responsible ownership can reduce insurance costs.

Completing accredited boating safety courses often qualifies for discounts.

Installing security systems, fire suppression equipment, and bilge alarms improves risk ratings.

Maintaining documented hurricane preparation plans reduces storm exposure.

Keeping detailed maintenance records demonstrates reliability.

Bundling policies may provide additional savings.

Selecting higher deductibles lowers premiums.

These steps can significantly reduce annual costs.

Most Florida yacht policies include hurricane provisions.

These clauses typically require:

Failure to follow hurricane protocols may void coverage.

Preparation before hurricane season is essential.

Many first time buyers underestimate insurance complexity.

Common mistakes include:

Avoiding these mistakes protects your investment.

Well insured yachts retain value and attract serious buyers.

Lenders and marinas prefer fully insured vessels.

Strong coverage reduces financial risk and ownership stress.

Insurance allows owners to focus on enjoying their time on the water.

Most owners pay between $2,500 and $3,200 per year for comprehensive coverage.

Insurance is not required by law, but most marinas and lenders require it.

Yes, most Florida policies include storm coverage when protocols are followed.

Yes, but older boats may require surveys and higher premiums.

Only if offshore navigation limits are included in the policy.

Most claims result in higher future premiums.

Yes, most policies can be reviewed and changed annually.

Choosing the right yacht directly affects insurance costs, operating expenses, and long term value.

At Hanover Yachts, our team helps buyers select well built, insurable vessels that perform reliably in Florida waters.

We guide clients through ownership planning, insurance considerations, and long term protection strategies.

Phone: ( +1 305-452-0002)

Email: sales@hanoveryachts.com

Website: https://hanoveryachts.com/

Reach out today to explore available models and get professional guidance on yacht ownership.

+1 305-452-0002

sales@hanoveryachts.com

1915 SW 21st Ave, Fort Lauderdale, FL 33312